Vijayarajan & Associates - Capital Gains Tax in India: Rules, Holding Periods & Latest Updates [2024-25]

Learn about short-term capital gains (STCG) tax rules in India, revised holding periods, and latest updates under the Finance Act 2024. Stay informed and plan your investments wisely.

Difference Between Short-Term and Long-Term Capital Assets in India

| Short Term Capital Asset | Long Term Capital Asset |

| Any Capital Asset held by the Taxpayer for a period of not more than 24 months immediately preceeding the date of it's transfer | Any Capital Asset held by the Taxpayer for a period of more than 24 months immediately preceeding the date of it's transfer |

| However in case of Certain Assets* the period of holding taken to be considered is 12 months instead of 24 months | If transfer of Asset takes place before 23/07/2024 the period of holding to be considered will be 36 months** instead of 24 months |

*Certain assets specified are shares (equity and preference) which are listed in a recognised stock exchange in India, units of equity oriented mutual funds, listed securities like Debentures and Government securities, Units of UTI and Zero-Coupon Bonds.

**For Capital Assets being Unlisted shares of a Company and Immovable Property, the period of holding will be 24 months regardless of date of transfer.

The following assets will be considered as long term if it the holding period is more than the below and short term if the holding is less than the below:-

| ASSET | PERIOD OF HOLDING |

| Listed Securities | 12 Months |

| Unlisted Shares and Immovable Property | 24 Months |

| Other Capital Assets if transferred before 23/07/2024 | 36 Months |

| Other Capital Assets if transferred on or after 23/07/2024 | 24 Months |

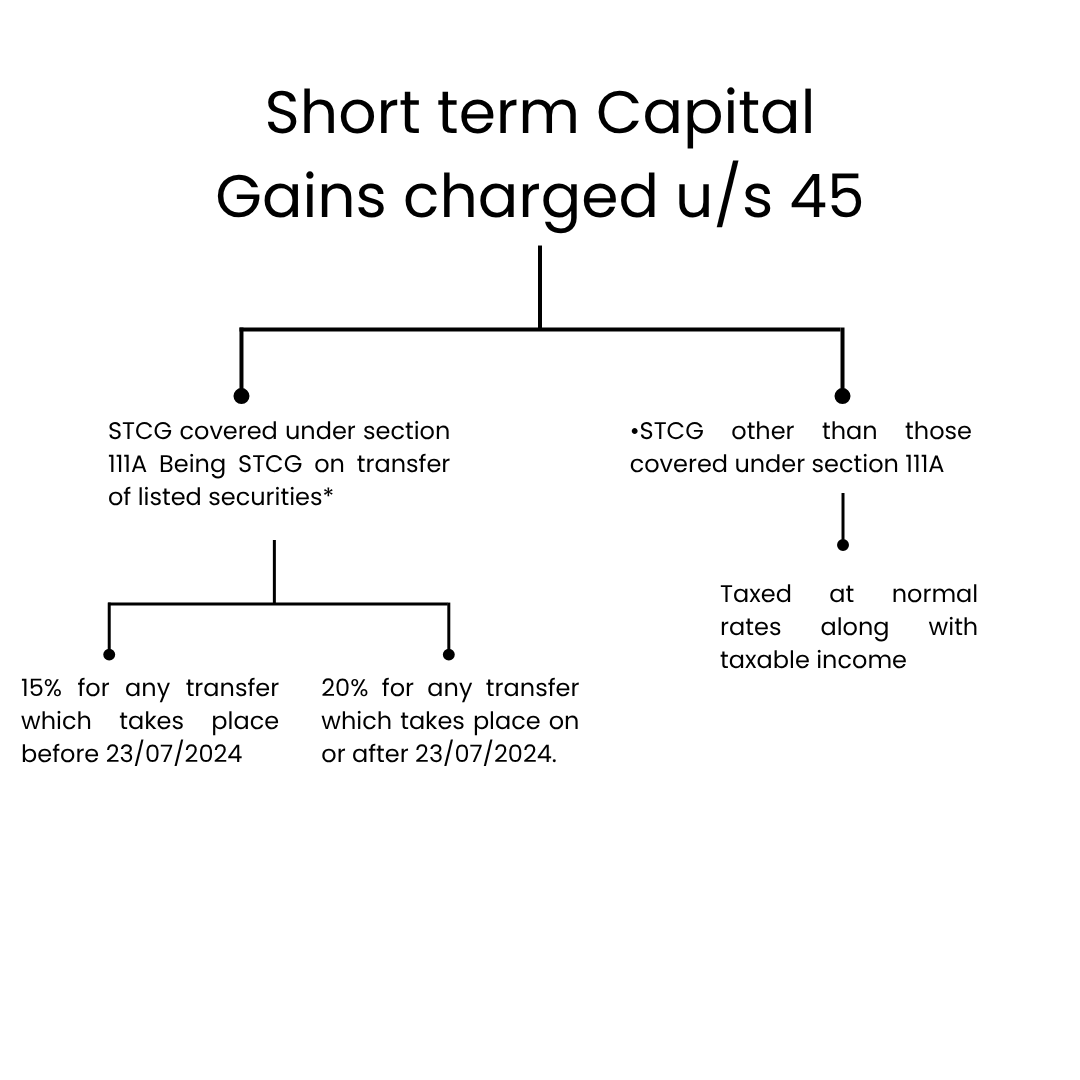

Short-Term Capital Gains (STCG) Tax in India – Section 45 & 111A Explained

Short-Term Capital Gains (STCG) refer to profits earned from the sale of a capital asset held for a short period (generally not more than 24 months). These gains are taxed under Section 45 of the Income Tax Act. The rate of taxation depends on whether the gain falls under Section 111A or not.

STCG Covered Under Section 111A

Section 111A applies to gains from the sale of:

- Listed equity shares

- Units of equity-oriented mutual funds [under section 10(23D)]

- Units of business trusts

This applies only if Securities Transaction Tax (STT) is paid on such transactions.

Applicable Tax Rates:

- 15% if the transfer occurs before 23rd July 2024

- 20% if the transfer occurs on or after 23rd July 2024

Note: The concessional tax rate of 15% is also available where STT is not paid, provided that:

- The transaction takes place on a recognised stock exchange in an International Financial Services Centre (IFSC)

- The consideration is paid or payable in foreign currency

STCG Not Covered Under Section 111A

If the short-term capital gain does not fall under Section 111A (e.g., gains from unlisted shares or immovable property), it is taxed at the normal slab rates applicable to the taxpayer and added to the total taxable income.

Other Important Provisions Related to STCG

- Basic exemption limit can be claimed on STCG not covered under Section 111A.

- For resident individuals and HUFs, the exemption limit can also be adjusted against STCG under Section 111A, but only after adjusting other income first.

- No deduction under Sections 80C to 80U is allowed from STCG covered under Section 111A.

- Deductions under Secions 80C to 80U can be claimed for STCG not covered under Section 111A.

Summary of Long-Term Capital Gains Tax Rates Under Sections 112 and 112A

| Section | Asset Type | Transfer Date | Tax Rate |

| 112A | Listed equity shares, units of equity-oriented funds or business trusts | Before 23-07-2024 | 10% on capital gains* |

| 112A | Listed equity shares, units of equity-oriented funds or business trusts | On or after 23-07-2024 | 12.5% on capital gains* |

| 112 | Unlisted securities or shares of a company (non-resident only) | Before 23-07-2024 | 10% on capital gains without indexation benefit. |

| 112 | Unlisted securities or shares of a company (non-resident only) | On or after 23-07-2024 | 12.5% on capital gains |

| 112 | Listed securities (non-unit) or zero-coupon bonds | Before 23-07-2024 | 10% without indexation benefit or 20% on capital gains with indexation benefit, whichever is less. |

| 112 | Listed securities (non-unit) or zero-coupon bonds | On or after 23-07-2024 | 12.5% on capital gains |

| 112 | Land and Building (acquired before 23-07-2024) – Resident Individual/HUF | Any | As per Special provision** |

| 112 | Land and Building – Others | Any | 20% on capital gain with indexation benefit. |

| 112 | Other assets (General Provision) | Before 23-07-2024 | 20% on capital gains with indexation benefit |

| 112 | Other assets (General Provision) | On or after 23-07-2024 | 12.5% on capital gains without indexation benefit. |

*Long-term capital gains exceeding 1,25,000 (in aggregate) will be taxable at the specified rates

**Special Provision for Long-Term Capital Gains on Land and Building

To provide relief to taxpayers from higher tax liability due to the amendments introduced by the Finance (No. 2) Act, 2024, a provision has been introduced for resident individuals and Hindu Undivided Families (HUFs).

- Applicability: For land or building acquired before 23rd July 2024, resident individuals and HUFs are allowed to opt for the old tax regime and continue to apply indexation benefits and pay tax at the earlier rate of 20%, if it results in a lower tax liability compared to the new rate of 12.5% without indexation.

- Tax Calculation Relief: If the tax payable under the new regime (12.5% without indexation) is higher than the tax computed under the old regime (20% with indexation), then the excess tax shall be ignored, and only the lower tax under the old regime will be levied.

Important Notes on Long-Term Capital Gains (LTCG) for Resident Individuals and HUFs

- Adjustment of Basic Exemption Limit:

- Only resident individuals and Hindu Undivided Families (HUFs) are allowed to adjust their basic exemption limit against long-term capital gains (LTCG). However, this benefit is available only after fully adjusting other income (excluding LTCG) against the exemption limit.

- In simple terms, the exemption limit first offsets income from sources like salary, business, or rent. Any remaining limit, if available, can be applied to reduce the taxable LTCG.

- No Deductions Under Chapter VI-A:

- Deductions under Sections 80C to 80U (such as investments in LIC, PPF, ELSS, etc.) cannot be claimed from long-term capital gains. LTCG is excluded from the benefit of these deductions.

Cost of Acquisition for Listed Shares Acquired Before 1st February 2018 (Grandfathering Rule)

To protect taxpayers from excessive tax liability due to rising stock prices prior to the introduction of LTCG tax on listed shares in Budget 2018, the Income Tax Act provides a grandfathering mechanism for equity shares acquired before February 1, 2018.

In such cases, the cost of acquisition is deemed to be the higher of the following:

- a) The actual purchase price of the asset, or

- b) The lower of:

- (i) The Fair Market Value (FMV) as on January 31, 2018, or

- (ii) The actual sale consideration received upon transfer

Definition of Fair Market Value (FMV):

- For listed equity shares, FMV is the highest price quoted on a recognised stock exchange as on 31st January 2018.

- If there was no trading on that date, the highest price of the share on the nearest earlier date on which it was traded will be considered as FMV.

- For unlisted units (such as certain mutual funds), the Net Asset Value (NAV) as on January 31, 2018 shall be deemed to be the FMV.

No comments yet. Login to start a new discussion Start a new discussion